Measuring profitability of a company

The content of this article

A company with good financial viability is a company that makes a profit. In other words, its income is higher than its expenses. However, to get a correct estimation of a company’s financial viability, the profit needs to be viewed in relation to several items in the income statement and balance sheet.

Financial viability can sometimes be relative. For example, a company should not be considered profitable if the business operation makes a smaller profit than what other alternative investments would have brought in.

Financial viability = A company’s ability to make a profit

Different Key Performance Indicators for Financial Viability

The key performance indicators that are used to describe a company’s financial viability can be divided into two categories. Both indicators answer the question of how profitable the company is – but from different perspectives.

Income Statement

It is easy to find indicators in the income statement. You can for example calculate:

Gross margin – The difference between purchase cost and total sales.

Profit margin – Profit before interest expenses divided by net sales

Net margin – Net result after financial items divided by net sales.

It is important to note that these indicators can be affected by the company by using various accounting methods. To create a clearer picture, the items from the income statement must be viewed in relation to items in the balance sheet.

Income Statement in Relation to Balance Sheet

The second category is the relationship between different items in the income statement and balance sheet. With these key performance indicators, the reason behind the financial viability and the effectiveness on managing capital and assets becomes clearer. It is at this stage that the term profitability is used.

Profitability

Profitability is the same as net income. If you choose to invest money in a savings account with 1% interest, the profitability of the investment is 1%. It shows how many percentages your investment has increased.

Profitability = Net Income

When profitability is used to calculate key performance indicators, at least one item from both the income statement and the balance sheet is used. It gives you a much more correct measure of the profitability than if you only look at the income statement.

Example:

Bob’s Construction Company has equity capital of $40,000 and borrows $60,000. Goods are purchased for $100,000 and are sold for $180,000.

The company has made a net profit of $80,000. But what is the profitability? Is it 80% (profit in relation to expenses) or 133% (profit in relation to equity capital)? By using different indicators the profitability can be explained better.

ROE – Return On Equity

ROE = Net Income / Equity

- Equity = Difference between the company’s assets and liabilities.

Profitability in relation to equity shows the net income that shareholders will receive from the added capital. 10% is often used as a rule of thumb, which means that a key performance indicator that is larger than 10% shows good profitability.

ROA – Return on Assets

ROA = Income before taxes + interest expenses / total assets

- Interested expenses = Expenses for interest-bearing liabilities

- Total assets = The value of the company’s fixed and current assets.

Profitability on total assets shows how effectively the company is at making profit on its total assets. It can be compared with what interest that is given on the assets, no matter if it is equity or loans. Interest expenses are included here. If the ROA is at 1% you could just as well put the money in a savings account.

Example – ROA vs ROE

John’s Construction Company has equity capital of $40,000 and has borrowed $90,000. During the year, John has bought products for $100,000 and sells them for $260,000. That is $160,000 profit.

ROE – Return on Equity = 160,000 / 40,000 = 4

ROA – Return on Assets = 160,000 / 1,300,000 = 1.23

As you can see, it matters greatly what kind of indicators you use in the calculation.

ROCE – Return on Capital Employed

Return on Capital Employed = (Operating profit + Financial income) / Capital employed

- Financial Income = Interest and dividends

- Capital Employed = Equity + interest-bearing liabilities

Return on Capital Employed shows the company’s profitability with the capital currently accessible within the company.

ROOC – Return on operating Capital

Operating profit / Operating Capital

- Operating Capital = Balance sheet total – liquid assets, financial income and non-interest-bearing liabilities

Return on Committed Capital is used to show the company’s profitability with financial assets and other financing deducted. In some cases ROOC gives a clearer picture of a company’s profitability than operating profit. This is especially true when financial assets are very large.

ROIC – Return on Invested Capital

ROIC = Profit + Fixed assets – Cash

ROIC is used to show the profitability in relation to the assets that can be used to make profit. This key performance indicator can for example be used industrial companies with large amounts of fixed assets. How effective is the company in creating profit with these assets?

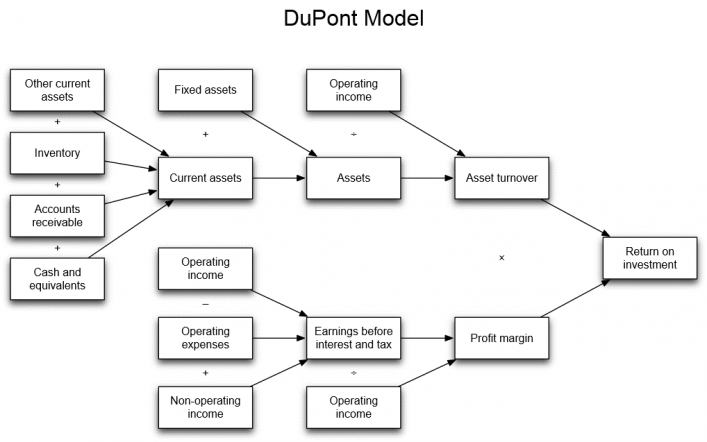

DuPont Model

Return on total capital (capital employed) = Profit margin * capital turnover ratio

The DuPont model is used to show profitability and what the company needs to improve to increase profitability. It is more advanced way to use many different indicators and put them in relation to each other.

Comparing profitability

As an investor the goal should be to buy stocks in companies who can make a profit – or in companies who has the potential to make a profit. But what is good profitability? First of all, it depends a lot on the industry. It is therefore important to compare a company’s key figures with similar companies within the same industry.

Example:

Capital-intensive industries have lower ROA – and vice versa.

Low turnover ratio should mean high margins – and vice versa.

Highly leveraged companies and/or companies with low solidity gets a higher ROE – and vice versa.

To analyze whether a company has a high profitability or not, you can use these key performance indicators to:

- Compare the company’s historical development

- Compare the company’s profitability with similar companies within the same industry

- Get a solid ground for further analysis – see the next heading

Profit in the short or long term?

Profitability starts with only one income statement and/or balance sheet and does not care about the reason behind the company’s result.

A company that commits a large portion of its capital for a year, to educate its personnel, may get a lower profit and therefore low profitability. But this education may lead to more complex services and higher prices, which in turn gives long term profitability.

It is therefore important not to stare blindly at the key performance indicators when measuring profitability. It is equally important to understand what lays behind these figures and how it may affect profitability in the future.